A comprehensive new report on the global gaming industry reveals significant trends, growth projections, and challenges facing the sector. The analysis examines player demographics, spending habits, device usage, and emerging business dynamics. While the industry shows strong growth potential, it faces hurdles including flat console adoption rates and workforce efficiency concerns.

Global Gaming Market to Hit $257 Billion by 2028

Key Insights

The 2024 industry analysis reveals the gaming sector's continued expansion and shifting player preferences.

- Market Growth: The gaming industry is projected to reach $257 billion by 2028, driven by consistent demand from a broad player base.

- Player Engagement: Younger players show heavy engagement, and those participating in game-related activities spend more on in-game content.

- Cross-Platform Compatibility: Player demand for device flexibility has made cross-platform play a priority for game studios.

- Console Market Stagnation: Console penetration has remained flat for a decade despite overall market growth.

- Mobile Gaming Risks: Smaller mobile gaming companies face high revenue volatility and substantial marketing costs.

- Workforce Efficiency: The expanding gaming workforce hasn't consistently translated to improved business performance.

Gaming Report 2024

Pay less for your games.

Get discounts up to 80% off

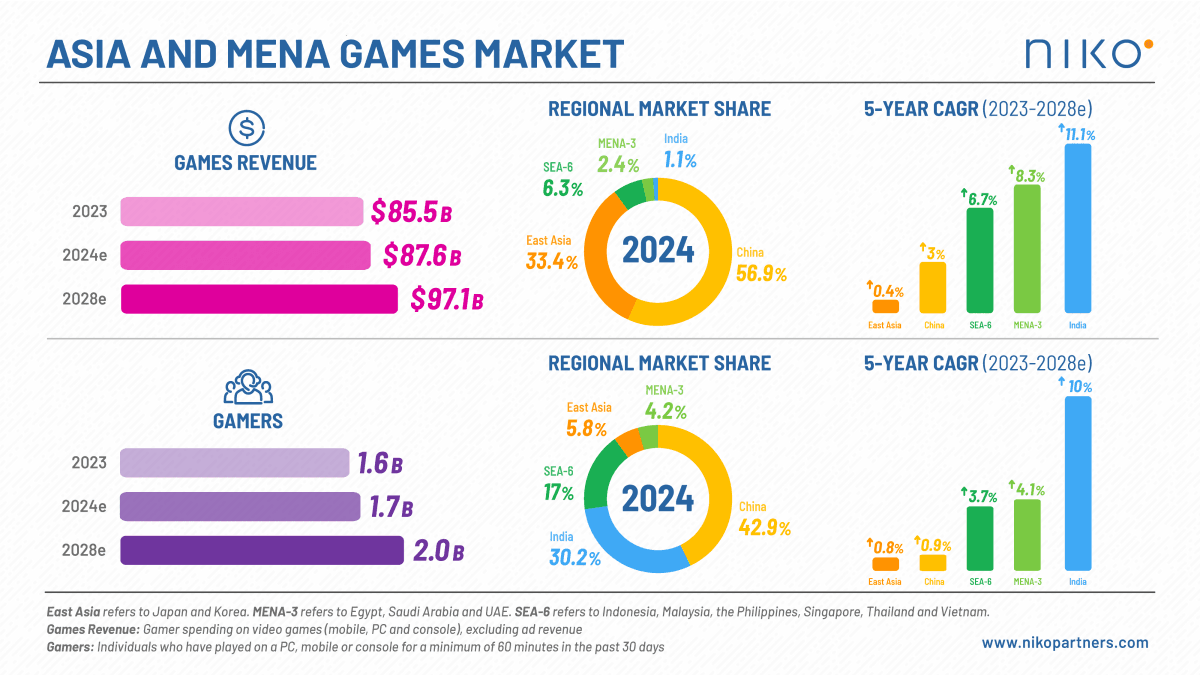

Industry Growth and Market Value

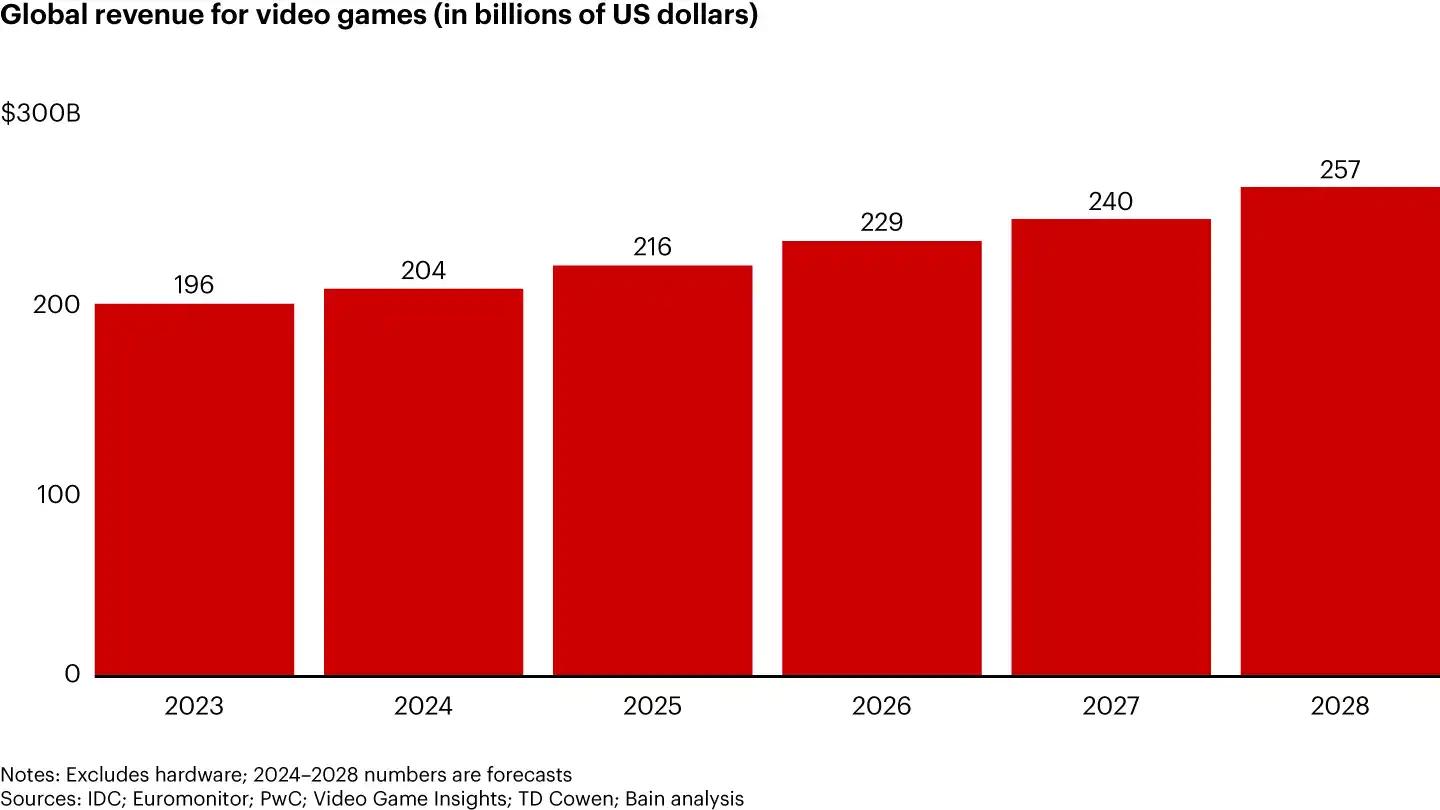

The gaming industry reached approximately $196 billion in 2023, exceeding the combined revenues of video streaming ($114 billion), music streaming ($38 billion), and box office earnings ($34 billion). Industry projections estimate an average annual growth rate of 6%, pushing the sector to $257 billion by 2028. This sustained expansion stems from an increasing base of engaged gamers, particularly among younger demographics who allocate significant portions of their budgets to gaming-related expenses.

Global Revenue fo Video Games (In Billions of US Dollars)

Gamer Demographics and Spending Behavior

A survey of over 5,000 respondents from six countries reveals a broad and diverse gamer population. Approximately 52% of respondents play games regularly. Young players (ages 2 to 18) show particularly strong engagement, with nearly 80% dedicating 30% of their leisure time to gaming. For older players (ages 45 and above), this engagement level drops to 31%.

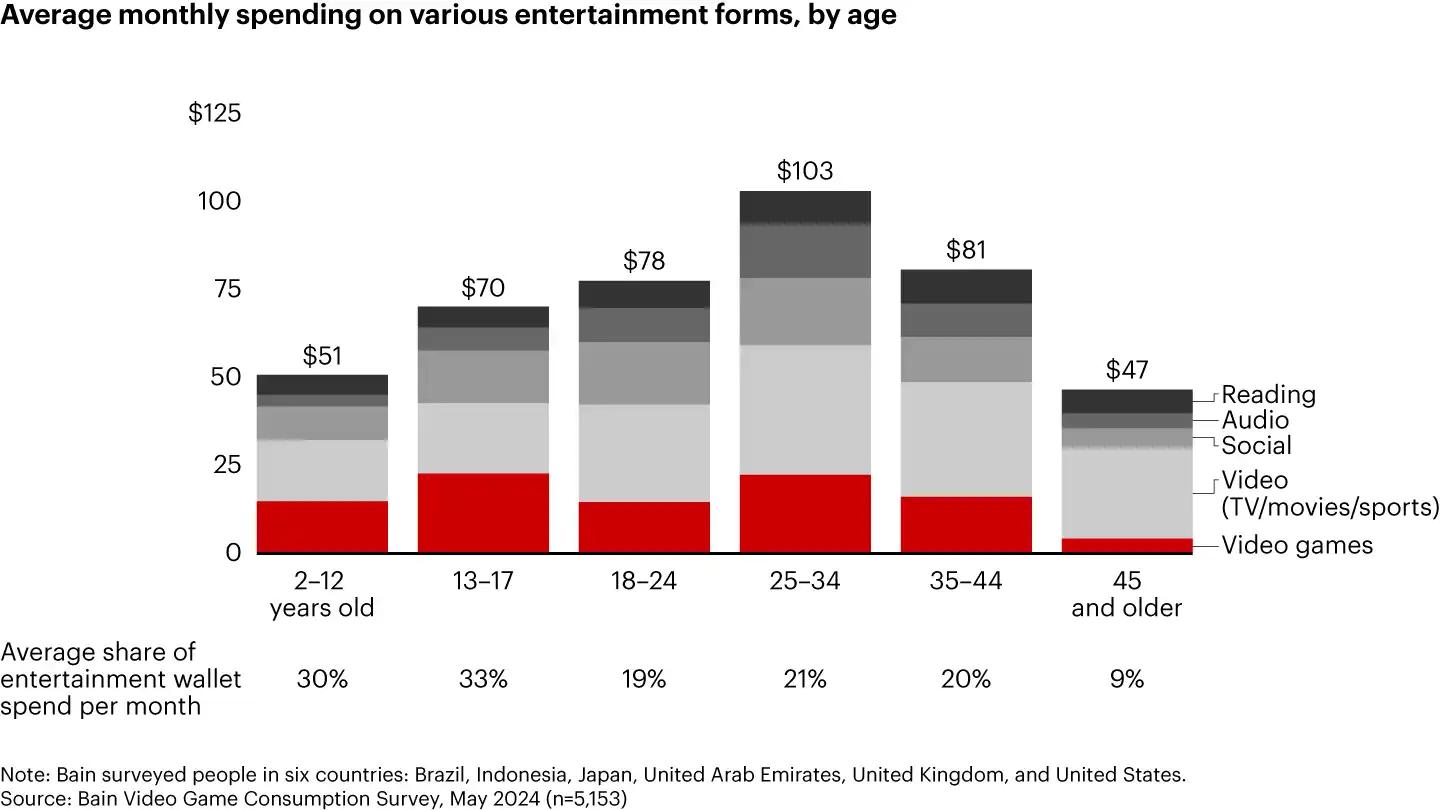

Players between 25 and 34 lead in spending, allocating the highest amounts on gaming and entertainment overall. Gamers increasingly engage in related activities beyond playing, such as socializing within game communities, watching gameplay videos, and purchasing game-themed merchandise. This broader engagement correlates with higher in-game spending, with players active in these secondary activities showing elevated expenditure patterns.

Average Monthly Spending on Various Entertainment Forms (By Age)

Device Usage and Cross-Platform Play

Nearly 70% of gamers use multiple devices for gaming, reflecting preferences for flexibility and accessibility. Cross-platform compatibility has become increasingly important, with 48% of players prioritizing the ability to play with friends across different platforms and maintain progress across devices. This demand has influenced game studios—95% of those with over 50 employees currently work on cross-platform support, aligning with broader shifts in player expectations for accessibility and continuity.

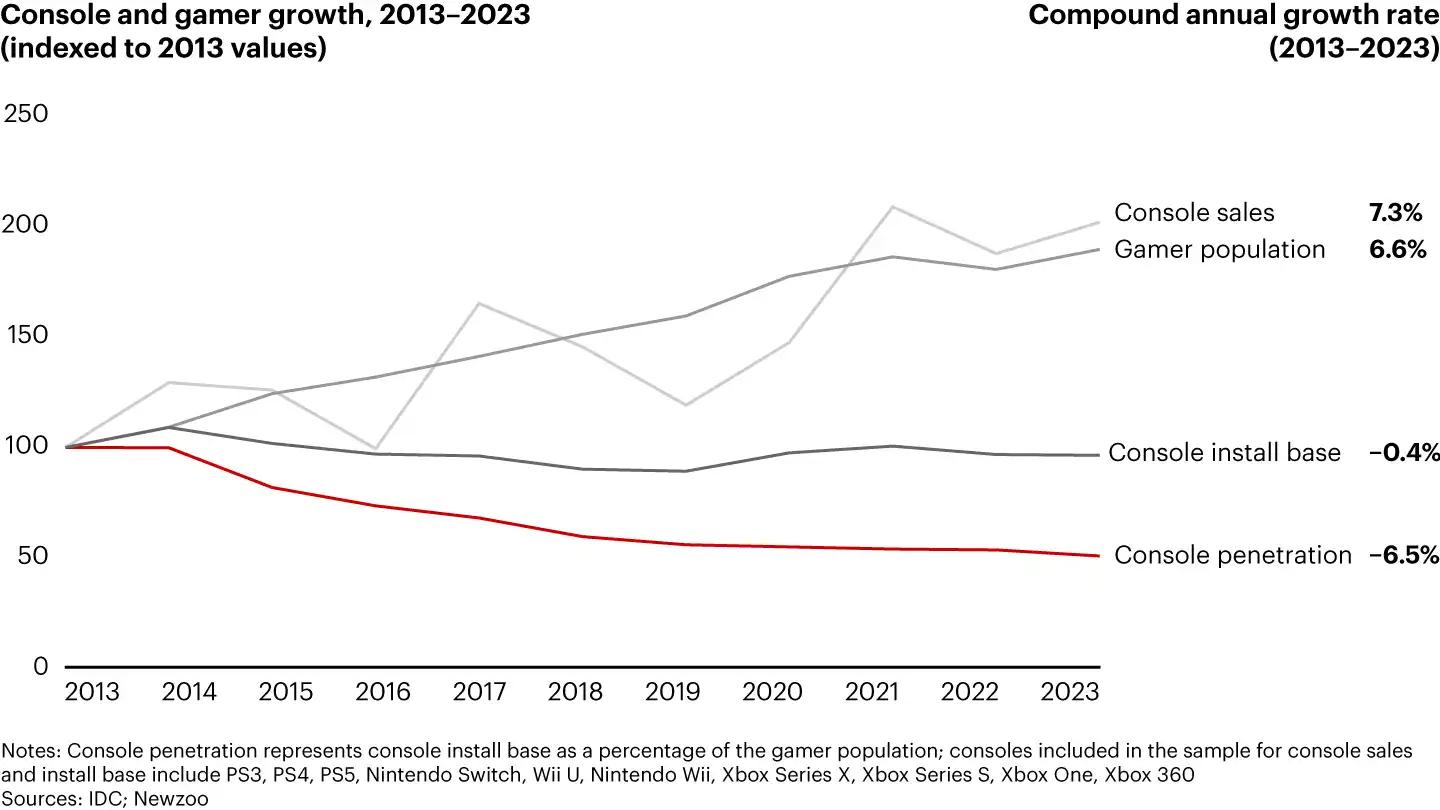

Console And Gamer Growther 2013-2023 (Indexed to 2013 Values)

Console Penetration and Content Consolidation

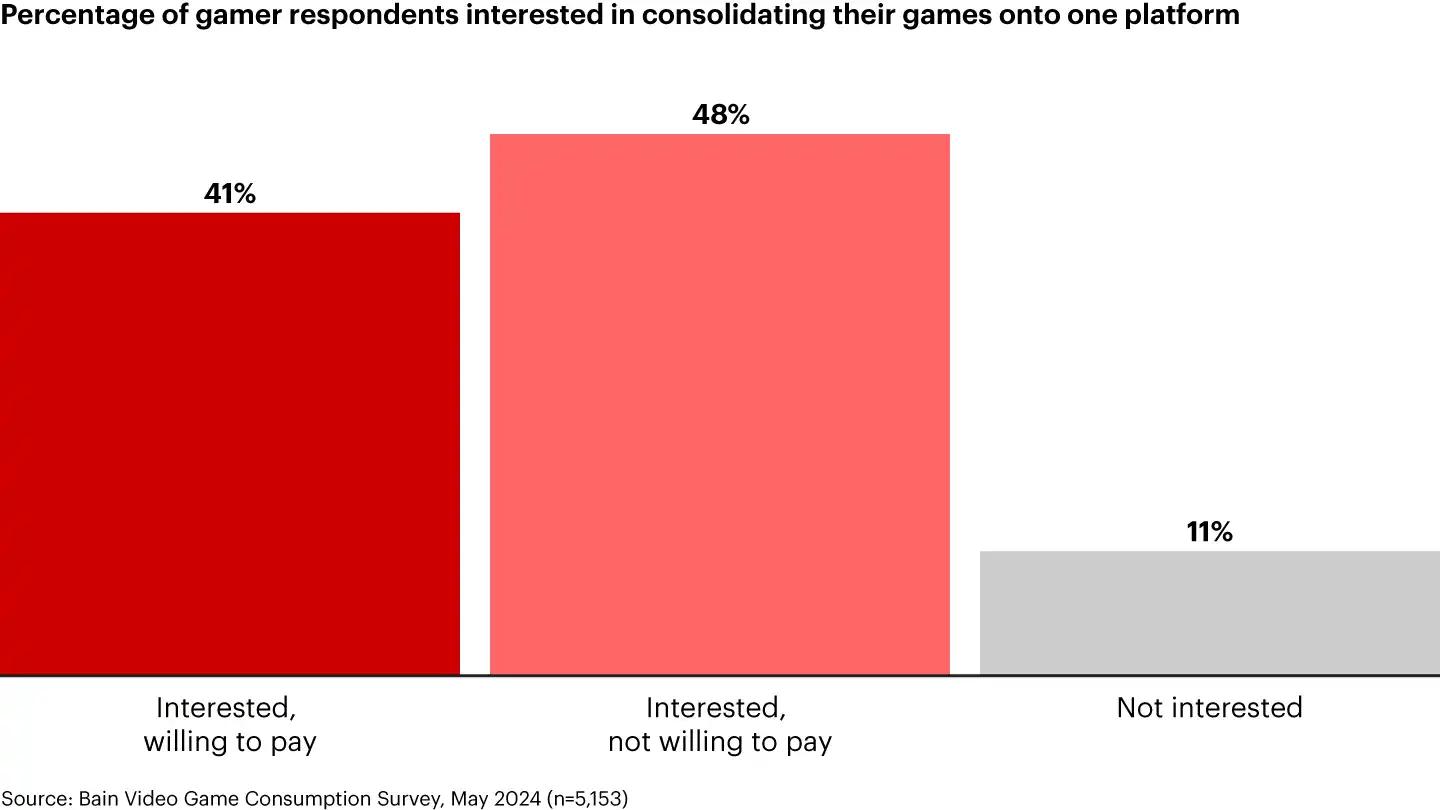

Despite gaming market growth, console penetration has remained unchanged over the past decade. This static penetration rate indicates that while the gaming audience continues to grow, it hasn't led to an equivalent increase in console adoption. The data reveals that 41% of gamers are interested in a single platform to consolidate game content, though only a subset is willing to pay for this feature—48% express interest but unwillingness to pay.

Percentage of Gamer Respondents Interested in Consolidating

Mobile Gaming and Marketing Dynamics

The analysis highlights unique challenges in mobile gaming, particularly for companies with annual revenues below $10 million. Small gaming firms in the mobile market face a 55-70% likelihood of revenue decline over a three-year period, significantly higher risk compared to other industries like software development (10-20%) or retail (10-25%).

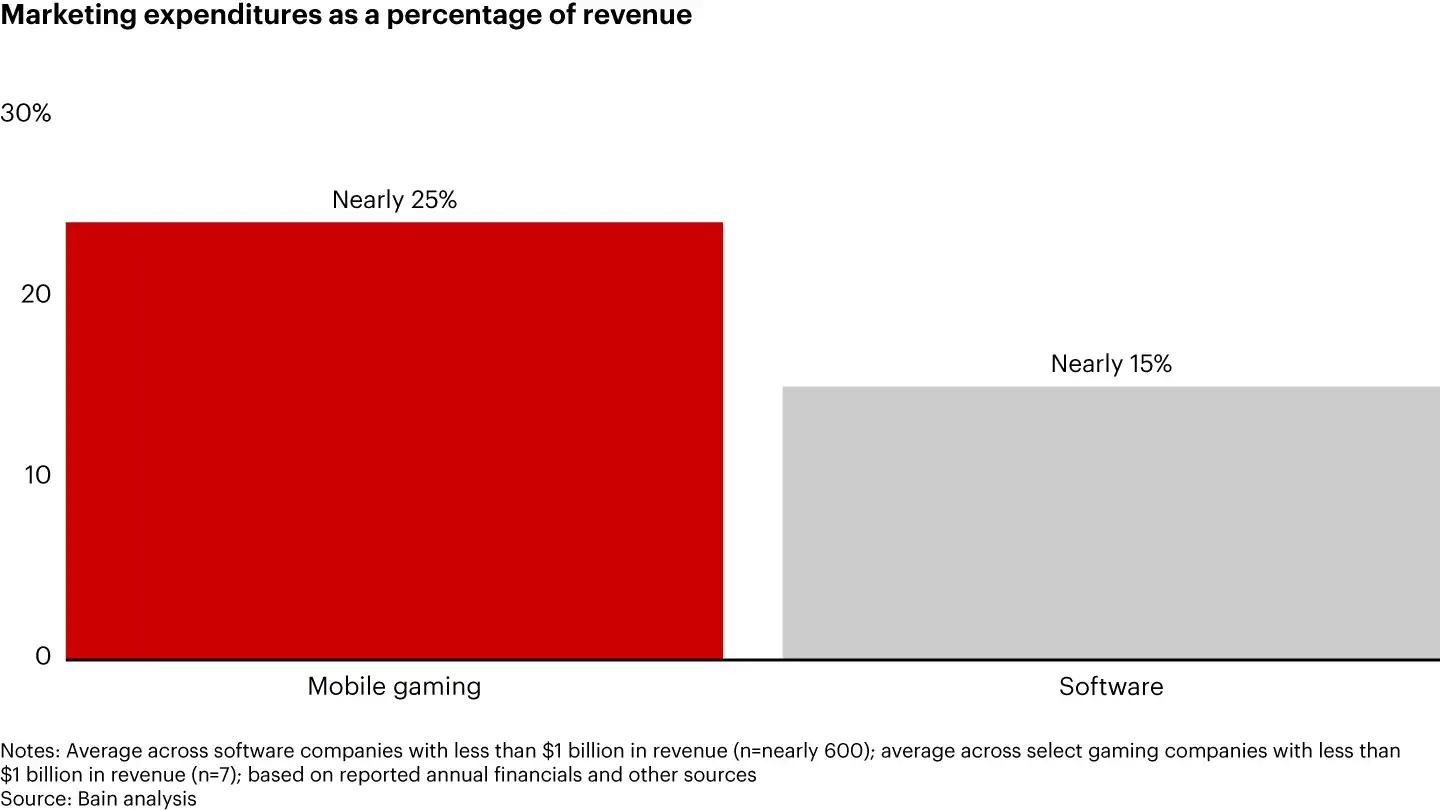

Marketing expenditures represent another critical factor in mobile gaming. Companies with less than $1 billion in annual revenue allocate approximately 25% of their budgets to marketing, substantially higher than average software industry spending. Mobile gaming companies that fail to capture and retain players often struggle to maintain revenue levels due to the competitive and high-turnover nature of the mobile gaming market.

Marketing Expenditures as a Percentage of Revenue

Workforce Growth and Changing Roles in Gaming

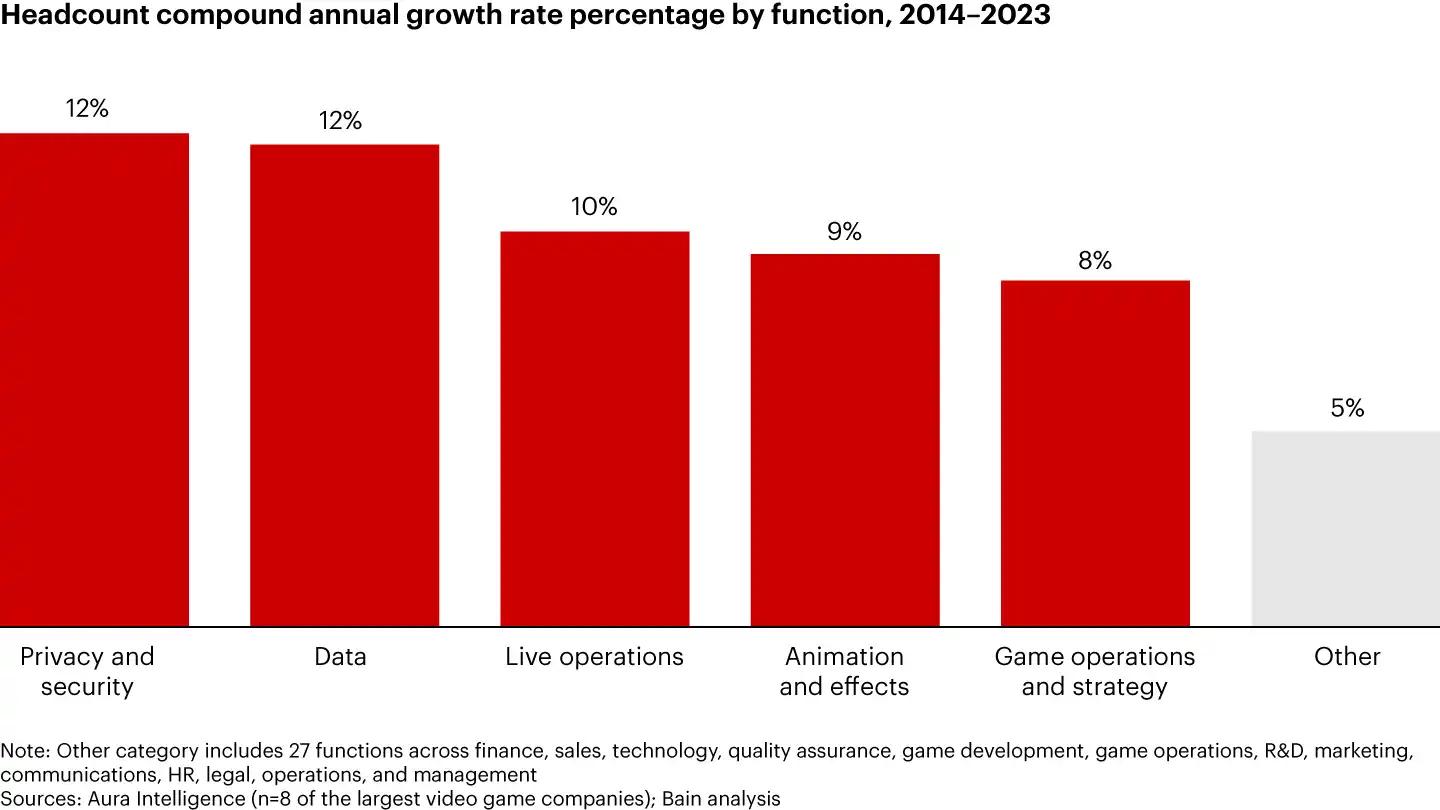

The past decade has seen shifts in staffing priorities of gaming companies, particularly in specialized roles. Positions in data, security, animation, LiveOps, and project operations have grown at twice the hiring rate of other roles. This trend reflects the industry's increasing complexity and need for specialists in areas crucial to modern game development and ongoing operations.

A concerning trend emerges in the weak correlation between workforce growth and business efficiency. Over the past 10 years, large gaming companies have experienced an average revenue growth rate of 6% annually, while their workforces have expanded by 7% per year. This discrepancy points to potential inefficiencies, as increased headcount hasn't consistently translated into enhanced business performance.

Headcount Compound Annual Growth Rate

Final Thoughts

The findings from this 2024 analysis highlight trends particularly relevant to the emerging web3 gaming space. As players increasingly seek cross-platform compatibility, ownership of digital assets, and community-driven experiences, web3 technologies such as blockchain and decentralized networks could offer compelling solutions. The insights on player engagement, particularly the value of social interactions, user-generated content, and secondary activities like digital asset trading, align with the core promises of web3 gaming: enabling true ownership, interoperability, and immersive communities.

The focus on mobile gaming's high-risk landscape underscores a potential opportunity for web3 models to mitigate revenue volatility through decentralized economies and player-to-player transactions. For web3 gaming developers and investors, this analysis underscores the potential for blockchain-based solutions to meet evolving player demands while addressing current industry challenges in engagement, monetization, and platform accessibility.