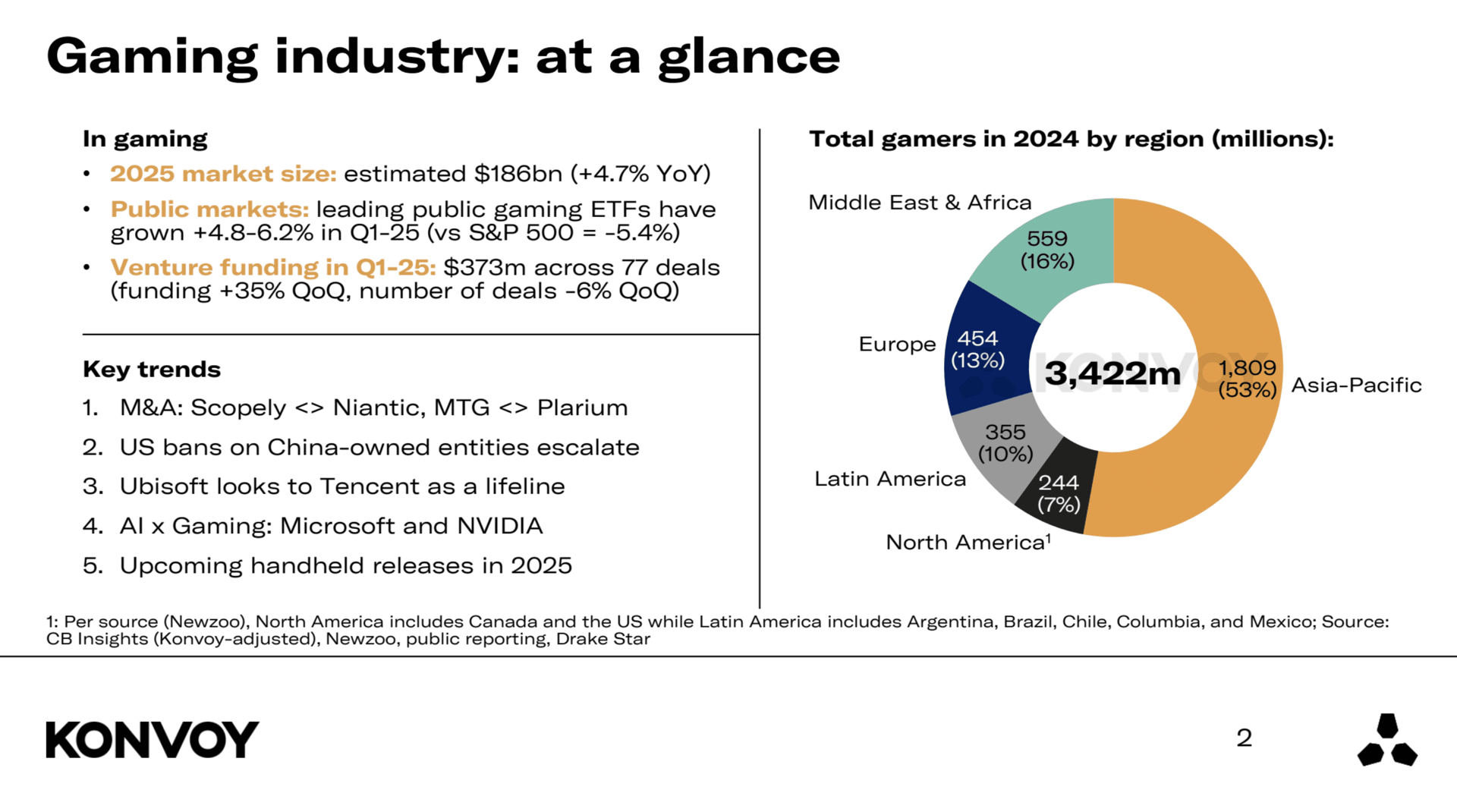

The global gaming market is projected to reach $186 billion by 2026, representing a 4.7% year-over-year increase. This moderate yet consistent growth reflects ongoing consumer engagement, expansion of digital distribution platforms, and the sustained relevance of gaming as a mainstream form of entertainment. Despite a dynamic macroeconomic environment, the industry continues to demonstrate resilience and stable forward momentum.

Konvoy Gaming Industry Report Summary Q1 2025

Investment Trends

The gaming sector pulled in $373 million in venture capital funding during Q1 2025. That's a 35% jump from the previous quarter, suggesting investors are warming back up after several quiet months. But zoom out to a year-over-year view and the picture shifts: funding is down 41% compared to Q1 2024, pointing to a more cautious investment environment overall. Deal count hit 77 for the quarter, down 6% from the prior quarter and 51% from the same period last year. Fewer deals but bigger checks means investors are being pickier about where they put their money.

Get 1-month GTA+ subscription with pre-order.

Pre-Order GTA 6 Now

Public Market Performance

Gaming-focused ETFs had a strong first quarter, outpacing broader market benchmarks. The ESPO ETF climbed 4.8%, while the HERO ETF gained 6.2%. Meanwhile, the S&P 500 dropped 5.4% year-to-date. That divergence shows publicly traded gaming companies held up better than the broader market, likely thanks to continued investor confidence in the sector despite volatility elsewhere.

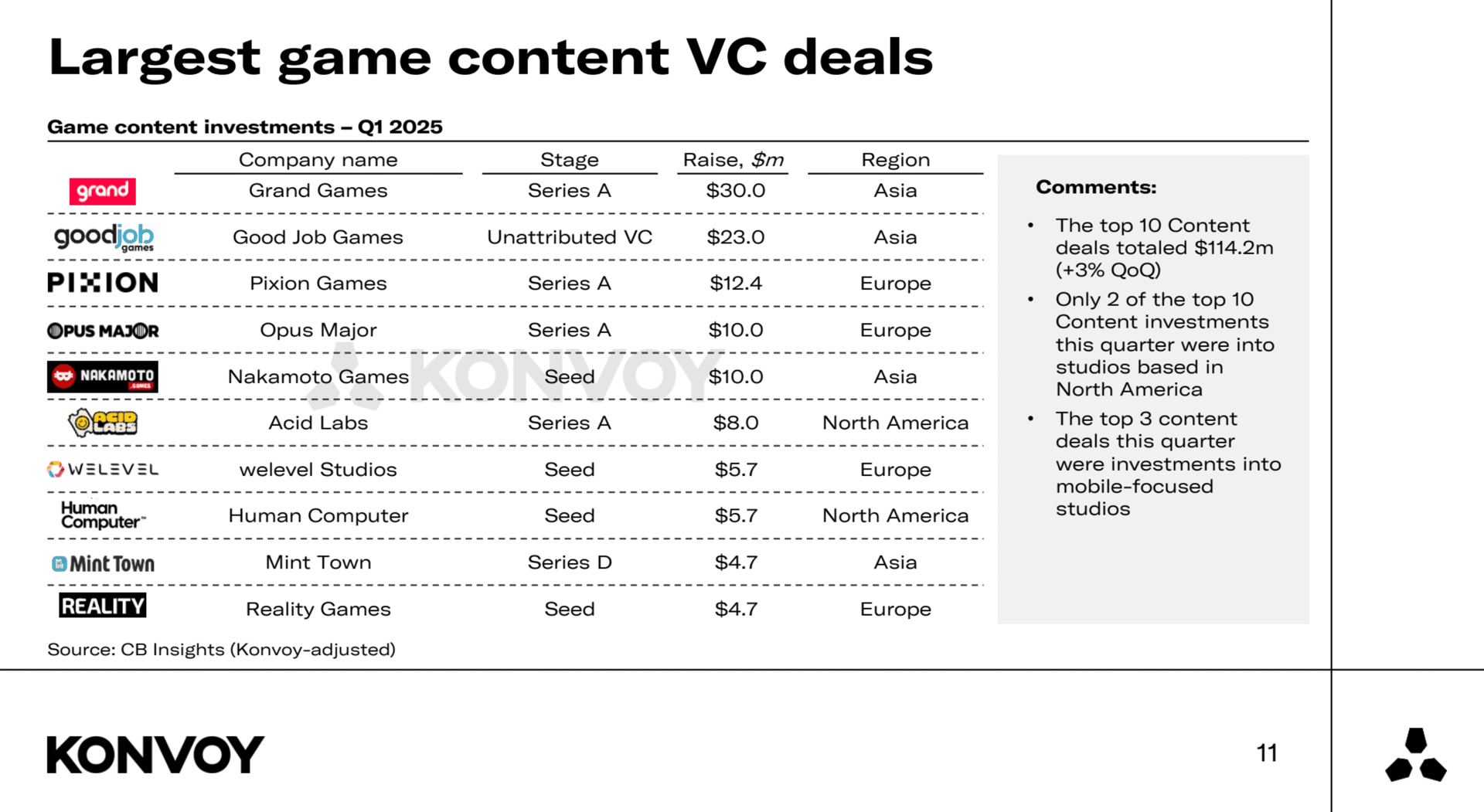

Largest Game Content VC Deals

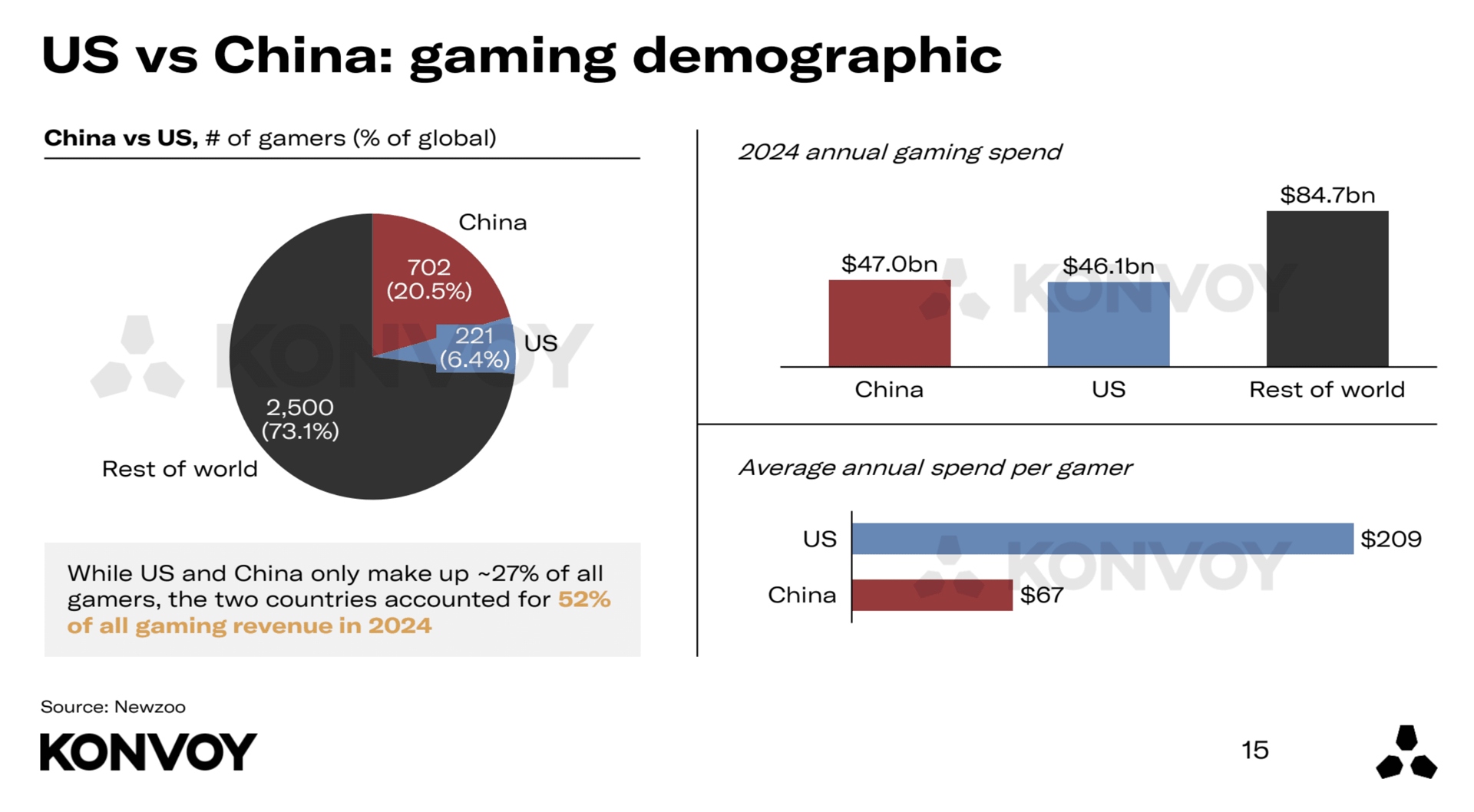

Regional Comparison: United States and China

The US and China remain the two biggest gaming markets, but their contributions look very different. In 2024, the US made up 6.4% of global gamers but generated 26% of global gaming revenue. China represented 20.5% of global gamers and also contributed 26% of revenue.

The average US gamer spends roughly 3.1 times more per year than the average Chinese gamer. US-based gaming startups also receive 7.6 times more venture capital funding than Chinese companies, and there are five times as many VC-funded gaming startups in the US. That points to a much stronger early-stage ecosystem on the American side.

US vs China Regional Comparison

Industry Consolidation and Strategic Restructuring

Q1 2025 saw several high-profile acquisitions. Scopely picked up Niantic, and Modern Times Group (MTG) closed its acquisition of Plarium. These deals reflect a broader trend: large gaming companies are consolidating operations and refocusing on their core strengths. The sales of Niantic and Plarium, along with rumors of AppLovin potentially offloading its gaming division, suggest companies are restructuring to sharpen their strategic focus and improve operational efficiency.

Geopolitical Influence on the Gaming Industry

Geopolitical tensions continue to shape the global gaming landscape, particularly around US regulatory actions targeting China-owned entities. The TikTok situation remains unresolved, with ByteDance receiving extended compliance deadlines. A full ban seems unlikely, especially since the platform resumed service for US users after a brief shutdown in January.

A consortium including Oracle, a16z, and Silver Lake is currently seen as the most likely buyer of TikTok's US operations. Broader scrutiny of Chinese gaming companies remains intense. Tencent-owned Riot Games and partially Tencent-owned Epic Games are among the entities potentially affected by further regulatory measures. Lilith Games, another Chinese firm, is also considered at risk under the evolving policy landscape.

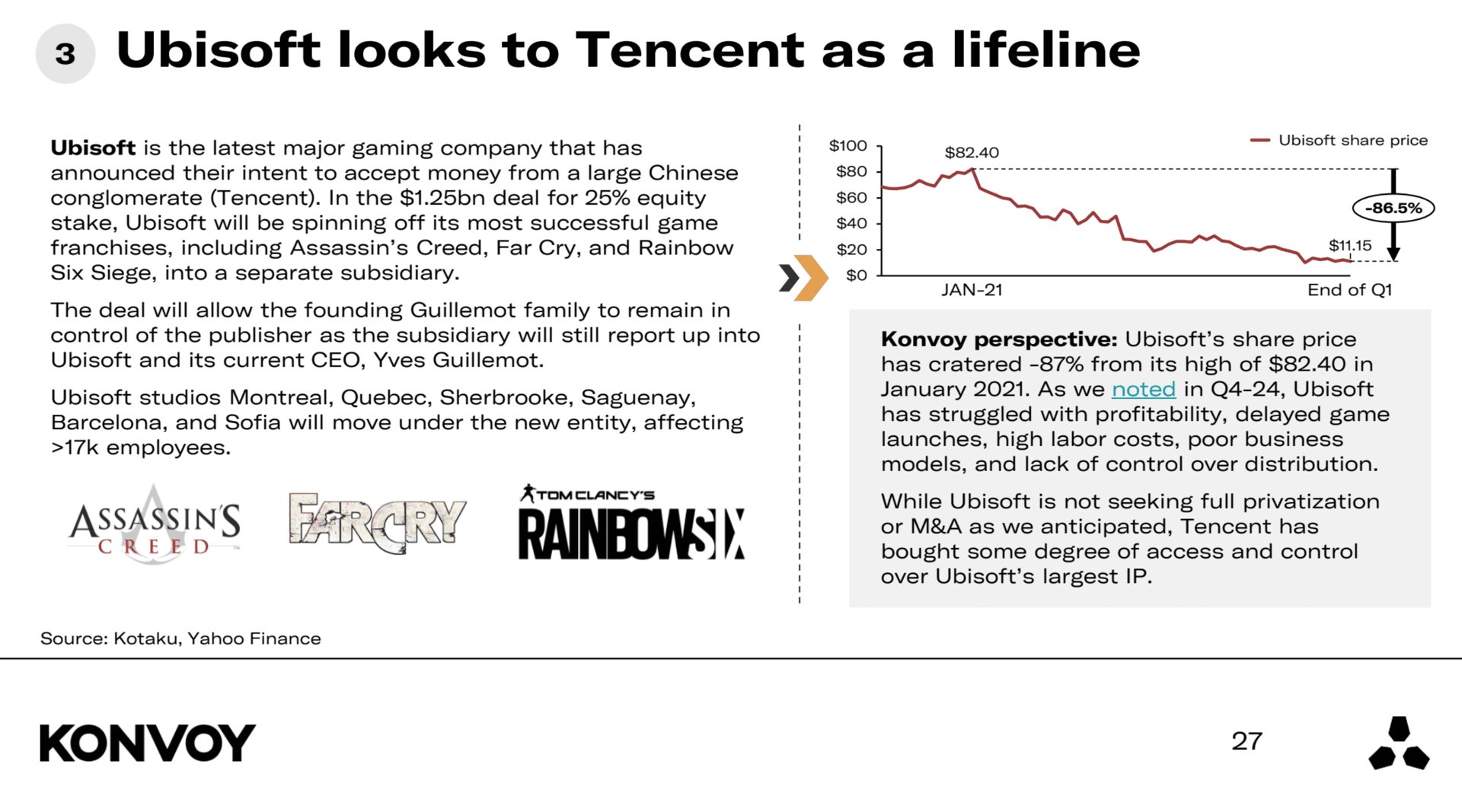

Ubisoft's Strategic Positioning

Ubisoft continues to struggle. Its stock price is down roughly 87% from its January 2021 peak. The company isn't actively pursuing full privatization or a merger, but Tencent has increased its influence over Ubisoft's intellectual property. That gives Tencent strategic access and underscores how critical IP control has become in the current gaming environment. Ubisoft's challenges have persisted for several quarters now and remain a major concern.

Ubisoft Looks to Tencent

Developments in AI and Gaming Technology

Artificial intelligence is playing a bigger role in game development. Microsoft recently launched MUSE, a model designed to speed up the early stages of game design through faster iteration and learning. Practical use cases for MUSE are still emerging, but the release signals Microsoft's ongoing interest in AI-driven tools for gaming. NVIDIA also introduced ACE, a platform built to support autonomous agents in games. The company has partnerships with NetEase, KRAFTON, and Wemade, though its long-term commitment beyond these initial deals isn't fully clear yet. These moves highlight the growing convergence of AI technology and interactive entertainment.

Upcoming Hardware Releases

Two notable handheld gaming devices are set to launch in 2025: the Switch 2 and the Atari Gestation Go. The Switch 2 follows Nintendo's massively successful original Switch, but projections suggest its hardware sales may underperform by 25 to 40 percent compared to its predecessor. The Atari Gestation Go is a retro-style device aimed at a niche audience, similar to nostalgia-driven products like the Atari Flashback Portable. It's unlikely to move the needle for the broader console market, but it reflects ongoing consumer interest in vintage gaming experiences.

The Q1 2025 snapshot shows a gaming industry navigating geopolitical and economic challenges while evolving through strategic investments, technology integration, and shifts in global market dynamics.