The African gaming industry is set to cross the $1 billion mark in 2024, driven by explosive mobile adoption and a young, digitally native population. Recent research from the Pan Africa Gaming Group (PAGG) and GeoPoll shows that 92% of gamers across the continent play primarily on smartphones, a clear signal of where the market's momentum lies.

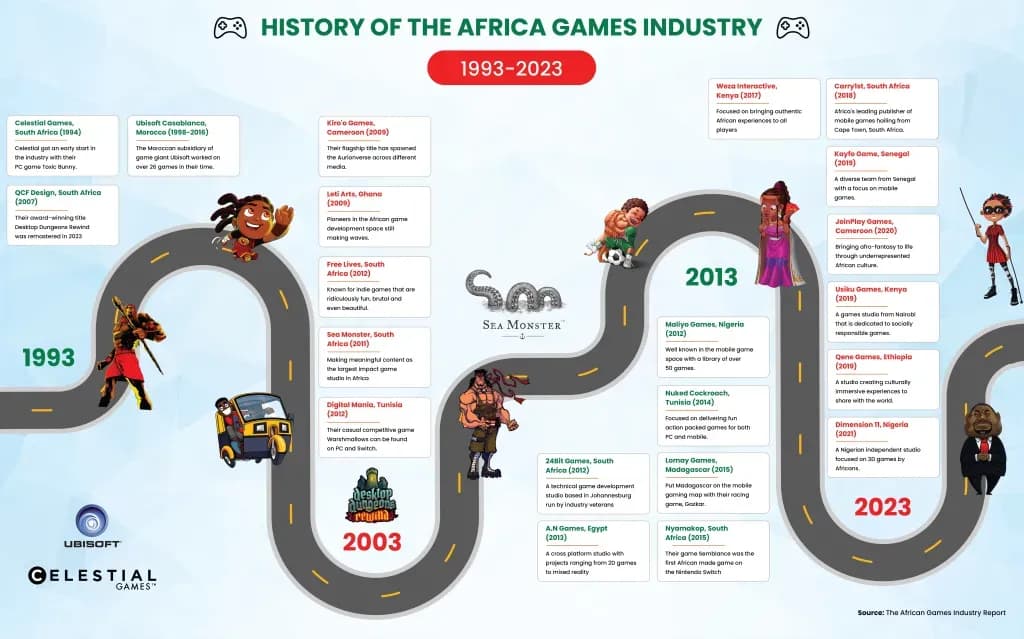

Nigeria-based studio Maliyo Games published its Africa Games Industry Report, detailing how 200 million gamers are spending hundreds of millions of dollars, almost entirely on mobile platforms.

Market projections indicate the African gaming sector will exceed $1 billion in consumer revenue for the first time this year. The GeoPoll and PAGG survey, along with Maliyo's findings, paint a picture of a fast-growing market with unique challenges and untapped potential. Here's what the data reveals for gaming and web3 enthusiasts.

GeoPoll and PAGG data

The GeoPoll report, unveiled at the Game Developers Conference, draws on responses from over 2,500 players in Nigeria, Egypt, Kenya, and South Africa. The results highlight player behavior, spending habits, and barriers to entry.

Mobile dominance: 92% of respondents play games on their phones. Smartphone penetration is rising fast, and Android is the platform of choice — 92% of players have downloaded games from the Google Play Store.

Engagement: Gaming is entertainment first. 73% play for fun, and 64% use games to relieve stress. It's a primary leisure activity, not a secondary one.

Spending: 63% of gamers have made at least one gaming-related purchase. 29% spend $2 to $5 per month. Players are willing to pay, but they're price-conscious.

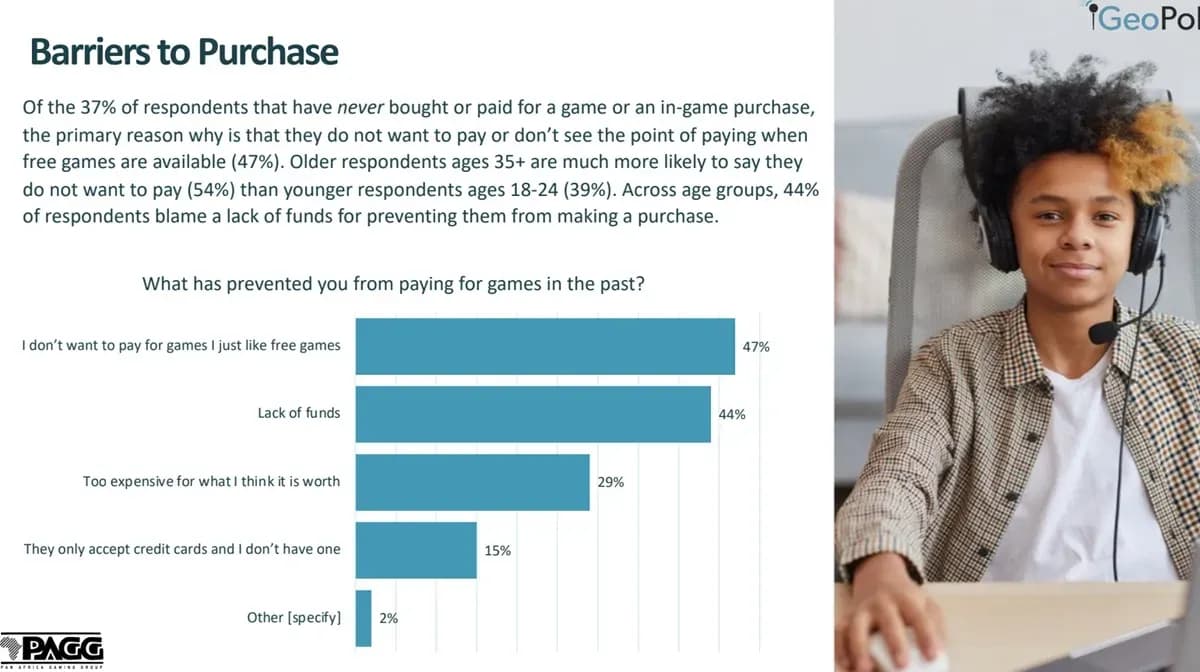

Barriers to spending: 47% prefer free games, and 44% cite lack of funds as a reason for not purchasing. Beyond game prices, 42% list the cost of data bundles as a major challenge, and 31% say gaming hardware is too expensive.

Cultural representation matters: Over half of respondents want games that reflect their culture. 44% feel there aren't enough games with characters or environments that resemble their own lives. This is a clear gap for local developers to fill.

In-game advertising works: Despite mixed feelings about ads, 63% of players have made a purchase after seeing an ad in a game. Ads may be intrusive, but they convert.

Local game visibility is low: 56% of respondents aren't aware of any games made in Africa. Local developers exist, but they're not reaching players. Interest in supporting local talent varies by country, but the demand is there.

John Murunga, GeoPoll's regional director for Africa, said the survey uncovered trends that highlight the sector's rapid growth and unique dynamics. He emphasized gaming's potential as a medium for cultural expression and community building across the continent.

Africa is the fastest-growing gaming market globally, fueled by a young, digitally native population and rising smartphone penetration. Jay Shapiro, chairperson of PAGG, noted that the data reveals the continent's billion-strong youth demographic as a massive opportunity for locally relevant games.

Newzoo and Maliyo Games data

Pay less for your games.

Get discounts up to 80% off

Market overview and spending

Market analysis from the Newzoo Global Games Market Report shows Africans spend an average of $6 per year on games, primarily through in-app purchases on mobile. Sub-Saharan Africa generates around $778.6 million in in-app purchase revenue, accounting for 90% of all game revenue in the region. South Africa leads with an average revenue per user of $12 annually. The African gaming market is projected to surpass $1 billion in consumer revenue by 2024.

Regional consumer spending breakdown

- Kenya: $46.5 million

- Ethiopia: $42.7 million

- Ghana: $34.6 million

- Côte d'Ivoire: $31.9 million

- Angola: $26 million

- Tanzania: $23.4 million

- Cameroon: $17.2 million

- Uganda: $16 million

Player population and audience

The Africa Games Industry report shows the number of gamers in Sub-Saharan Africa grew from 77 million in 2015 to 186 million in 2021. Mobile gaming accounts for 95% of the playing population (177 million). The top five gaming markets are Nigeria, South Africa, Ethiopia, Kenya, and Ghana.

The African gaming market is diverse, with over 3,000 distinct ethnic groups and more than 2,000 languages spoken across the continent. English, French, Swahili, Hausa, and Arabic are among the most widely used languages, presenting both challenges and opportunities for developers.

Demographics and growth potential

Africa has a median age of 19.7 years, and roughly 60% of the continent's 1.4 billion people are under 18. This demographic shift is increasing buying power, including spending on video games.

The Africa Game Developer Survey shows 78% of respondents are working on mobile games, 70% on PC games, and 18% on console games. Unity is the most widely used game engine at 64%, followed by Unreal at 14%. Financial challenges persist — only 59% of developers have secured external investment. Infrastructure issues like unstable power supply and unaffordable internet access remain significant obstacles.

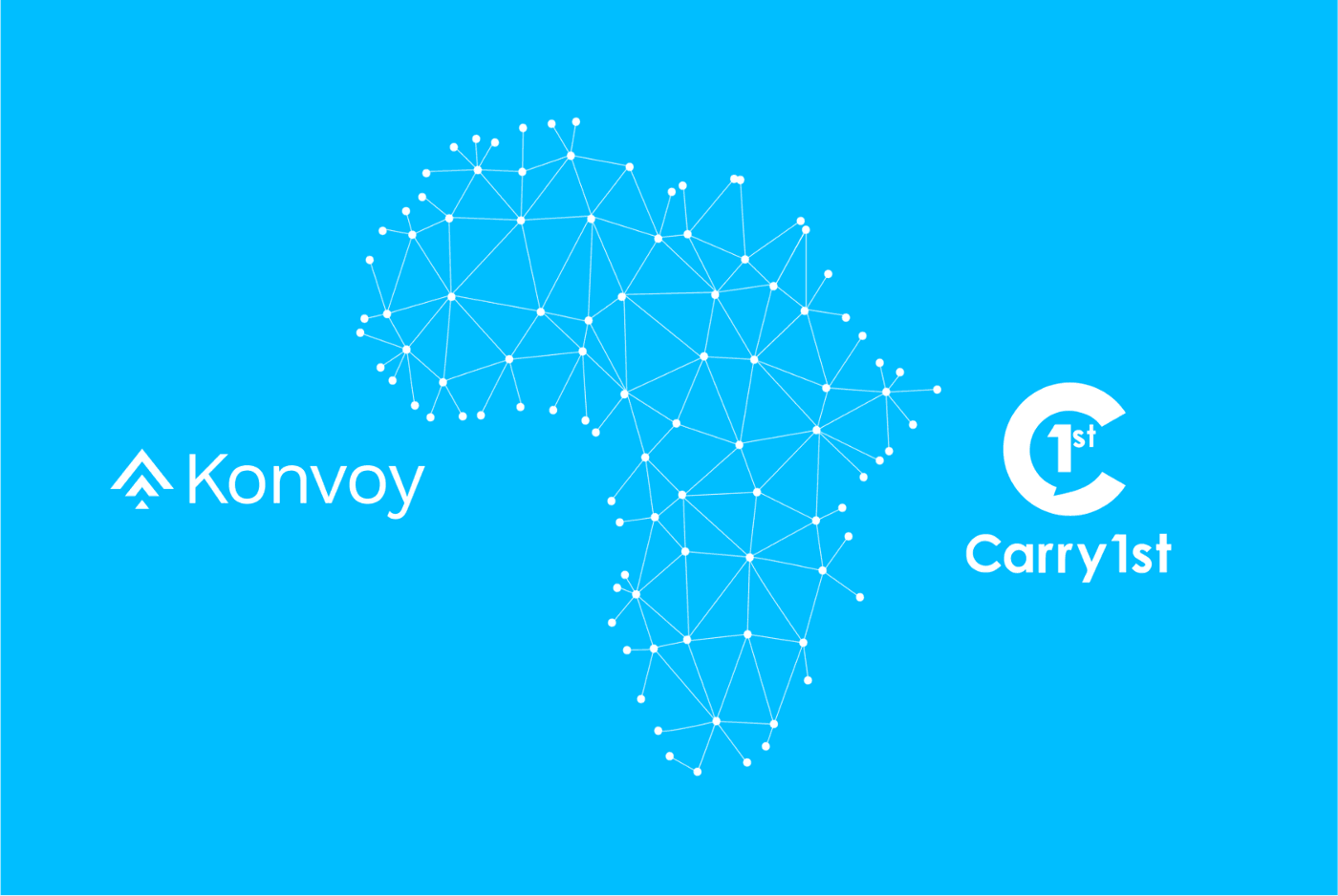

VC funding: Carry1st case study

With the number of gamers in sub-Saharan Africa projected to exceed hundreds of millions in the next five years, startups like Carry1st are positioning themselves to capitalize on the opportunity.

This South Africa-based publisher of social games and interactive content has raised substantial funding from investors including Andreessen Horowitz (a16z), Konvoy Ventures, and Bitkraft Ventures, which joined its $27 million pre-Series B round.

Africa is one of the fastest adopters of web3 technology globally. Data from the International Monetary Fund (IMF) shows crypto transactions from the region reached $20 billion per month in 2021. Alternative assets are popular in many African regions because mainstream fiat currencies are notoriously unstable.

Relevance to web3 gaming

These findings offer insight into how web3 gaming could fit into the African market. With 92% of players on mobile, accessibility and convenience are critical. Blockchain gaming, with its decentralized and interoperable structure, could eliminate the need for centralized app stores and enable seamless cross-platform experiences. This aligns with the mobile-first preference and could drive further adoption of web3 technology.

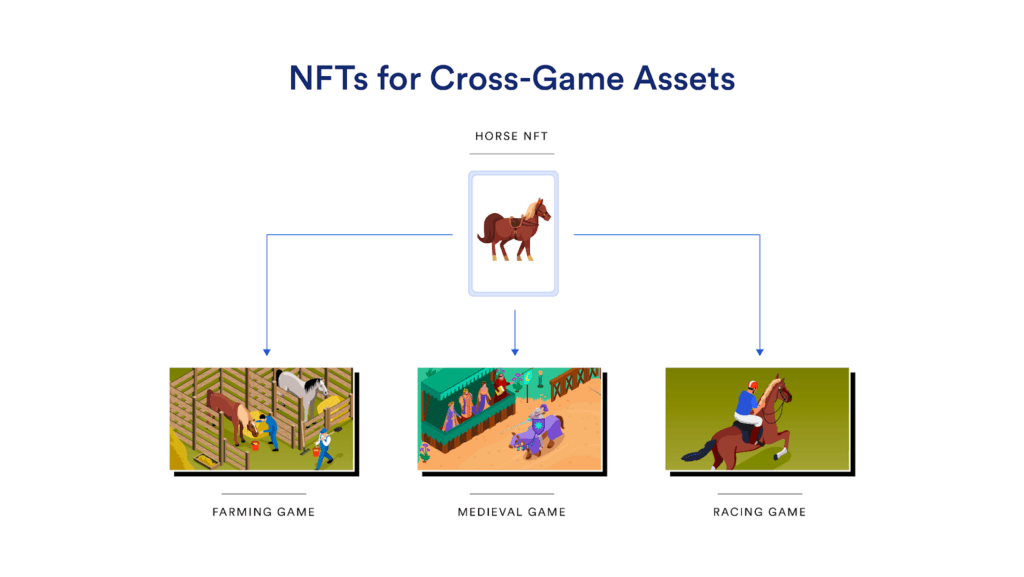

The data also shows 63% of gamers have made gaming-related purchases, highlighting the economic potential of the web3 gaming ecosystem. Decentralized finance (DeFi) mechanisms can introduce new monetization models like play-to-earn and non-fungible tokens (NFTs). These models allow players to own their in-game assets and participate in value creation within virtual economies, creating a more sustainable and inclusive gaming ecosystem.

The barriers identified — preference for free games and concerns about costs — are areas where web3 gaming could offer solutions. Through decentralized governance and tokenomics, web3 platforms can incentivize participation and reward players for their contributions, lowering barriers to entry and fostering a more inclusive community. Blockchain's transparency and immutability can also address concerns around data privacy and security, building trust among gamers.

Final thoughts

The African gaming market is growing fast, and the data underscores the potential for web3 gaming to reshape how games are created, distributed, and monetized. Decentralization, blockchain technology, and community-driven innovation could foster greater inclusivity, ownership, and engagement, opening the door to a new era of gaming experiences on the continent.