The 2025 AppMagic monetization report reveals a mobile games market still expanding, though growth has decelerated compared to previous years. Worldwide in-app purchase revenue climbed from $55.2 billion to $57.1 billion, with the App Store accounting for most of that increase through a 5.4% rise in spending. Google Play spending held roughly steady. Midcore and casual categories grew at a measured pace, while hypercasual and hybridcasual games nearly doubled their revenue year over year despite launching from a smaller baseline.

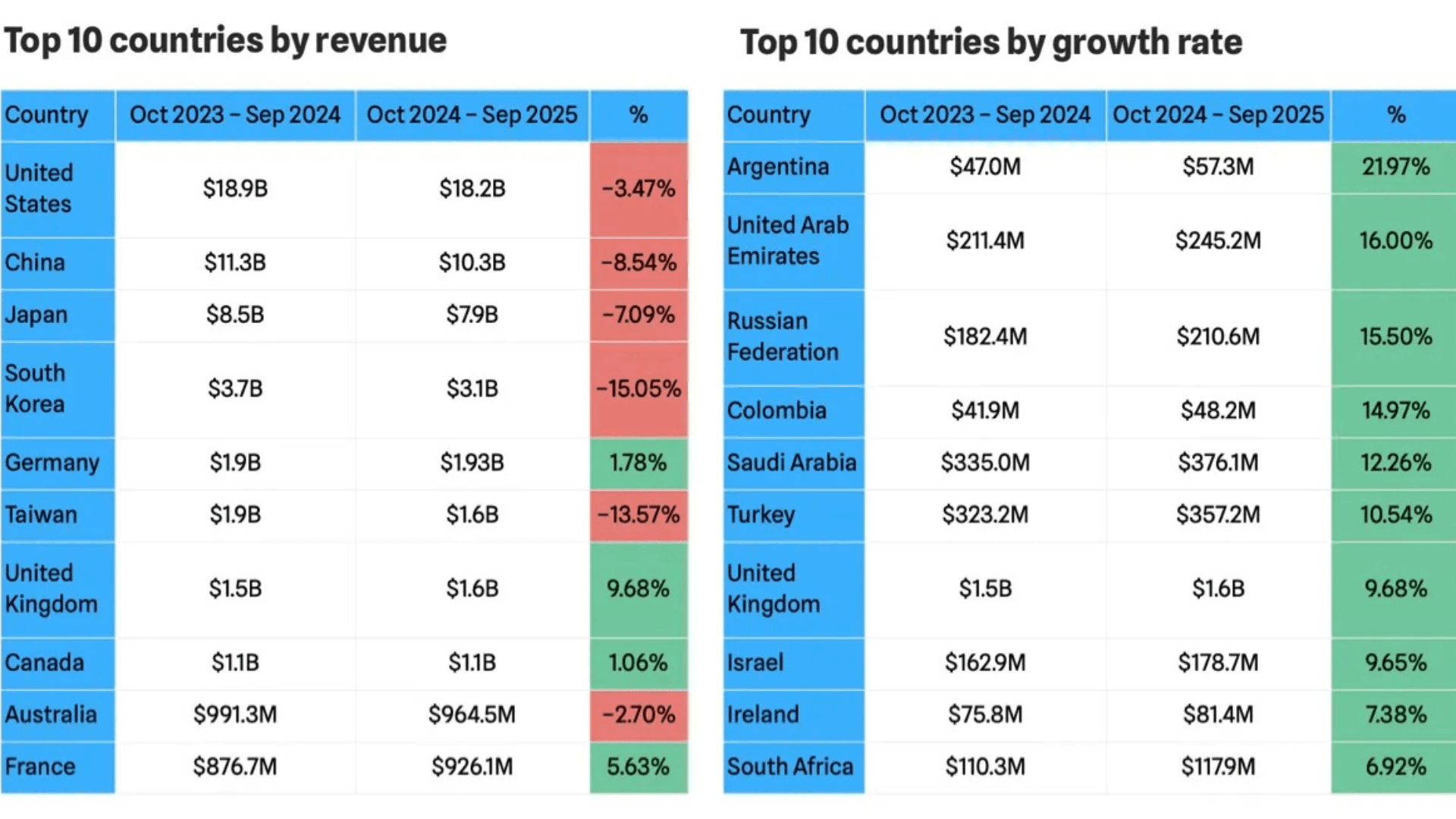

Regional results diverged sharply. The United States, China, Japan, and South Korea continued to generate substantial revenue, yet multiple Asian markets saw steep drops. At the same time, select European territories and emerging economies such as Argentina and the UAE posted significant gains. The data indicates that revenue expansion is gradually moving away from established hubs toward regions with greater economic volatility and currency instability.

Get 1-month GTA+ subscription with pre-order.

Pre-Order GTA 6 Now

The evolving role of alternative payment channels

Alternative payment integrations expanded further, with payment SDK adoption rising 12% since early 2024. Solutions including YooKassa, Xsolla, and Card.io gained the most traction, while Stripe, Paystack, and PayU usage declined. Integration activity peaked in summer 2024 before leveling off, and Samsung Pay removals spiked due to the discontinuation of Tizen support rather than broader market trends.

In the United States, D2C revenue among the top-grossing 100 games surged 46% year over year. Despite this, fewer titles now offer D2C options. The share fell from 72% in late 2024 to 62% in the first half of 2025, suggesting that while D2C spending is climbing, fewer top earners are maintaining these channels. Publishers that keep D2C systems active appear to extract more revenue from them even as overall adoption contracts.

Strategy titles post one of the year's strongest gains

Strategy titles saw one of the sharpest increases across major genres, with revenue reaching $13.5 billion in 2025. Both storefronts recorded meaningful growth, and subgenres like card battlers, tactical projects, and 4X strategy all posted significant gains. MOBAs were the only subgenre to decline. Much of the genre's revenue originates from Asian publishers whose initial gameplay loops often conceal more complex systems underneath.

U.S. player spending data shows that strategy players rank among the highest-value spenders on mobile. By day 90, spending per payer in strategy titles roughly doubles that of casino players. iOS users spend considerably more than Android users, frequently exceeding $15 per transaction, and high-value bundles such as $99 packs regularly appear among top revenue drivers.

RPGs face a sharp downturn

RPGs experienced one of the steepest declines in 2025. Revenue dropped from $13.7 billion to $11.6 billion, with both platforms posting similar declines. China recorded one of the most severe regional drops at 25%. Tactical RPGs and roguelikes provided rare positive signals, but most subgenres shrank.

Payment behavior in the United States reveals contrasting platform trends. On Google Play, both purchase frequency and ARPPU fell sharply. On the App Store, spending rose on both metrics, and first-purchase prices climbed to an average of nearly $18. Hard-currency bundles and large package offers continue to dominate revenue generation. Some RPGs are testing low-cost event bundles aimed at broadening conversion among non-paying players.

Puzzle games grow as new subgenres emerge

Puzzle games expanded from $7.7 billion to $8.8 billion, driven largely by App Store users. Several smaller subgenres surged, including Block Puzzle and Fill & Organize. Match-3 maintained steady growth, adding roughly $200 million year over year. Declines in Find the Difference and bubble shooters offset some momentum but did not stop overall category expansion.

Among the top U.S. puzzle titles, ARPPU edged down slightly and purchase frequency fell sharply on iOS. However, purchase values increased significantly, reflecting a shift toward higher-priced transactions. Most revenue now flows from LiveOps-linked offers priced between $6 and $15. Some developers are converting customizable bundles into recurring features to boost engagement and flexibility for paying players.

Casino spending declines across major markets

Casino games fell from $7.8 billion to $7.2 billion in 2025. The U.S. market dropped 11%, though the UK and Germany remained stable with modest growth. Bingo and card-based casino games posted small increases, but slots and Coin Looter games declined noticeably.

Payment activity weakened across both platforms. Google Play recorded sharp drops in ARPPU and purchase frequency, while iOS saw higher ARPPU despite fewer purchases. Currency bundles remain the primary revenue driver across the segment.

Simulation titles maintain consistent expansion

Simulation titles grew to $4.8 billion, supported mainly by the App Store. The revenue gap between iOS and Android widened further over the year. Sandbox games drove most of the genre's growth, while smaller categories such as work and animal simulators more than doubled from low starting points. Idol Training and fishing simulators declined.

In the United States, purchase frequency dropped, but iOS ARPPU increased while Google Play ARPPU fell. Purchase values rose sharply on both platforms, particularly on the App Store. Currency bundles remained the core revenue driver, accounting for more than 40% of spending in most top titles.

Hybridcasual posts the market's fastest expansion

Hybridcasual remained the fastest-growing category, climbing from $390 million to $733 million in 2025. The segment continues to evolve as developers add deeper gameplay systems and more sophisticated monetization to simple core loops. New hybridcasual titles are reaching top-grossing charts more frequently, demonstrating that the category remains competitive and accessible.

Payment data from the United States shows robust performance. Purchase frequency grew significantly on Google Play and more modestly on iOS, while ARPPU increased across both platforms. Purchase values declined on Google Play but rose on the App Store. Most revenue originates from low-priced currency bundles, limited-time loss offers, and seasonal passes.

Frequently Asked Questions (FAQs)

What were the biggest growth genres in mobile gaming in 2025?

Strategy, puzzle, simulation, and especially hybridcasual games saw the strongest growth, with hybridcasual nearly doubling year over year.

Why did RPG revenue drop so sharply?

RPGs saw major declines in key Asian markets, particularly China. Most subgenres contracted except for tactical RPGs and roguelikes.

Is D2C still growing in mobile gaming?

Yes. D2C revenue increased significantly, although fewer top U.S. games are using D2C tools compared to last year.

Which platform saw stronger monetization overall?

Across most genres, the App Store showed stronger ARPPU and higher average purchase values than Google Play.

What is driving hybridcasual growth?

Higher download volumes, deeper monetization, and increasingly complex gameplay systems are helping hybridcasual games reach top-grossing rankings.

Are players spending more or less per purchase in 2025?

It depends on the platform. iOS users are generally spending more per purchase across nearly all genres, while Google Play trends vary by category.